APY vs APR: What’s Key Differences?

Last Updated: October 9, 2024

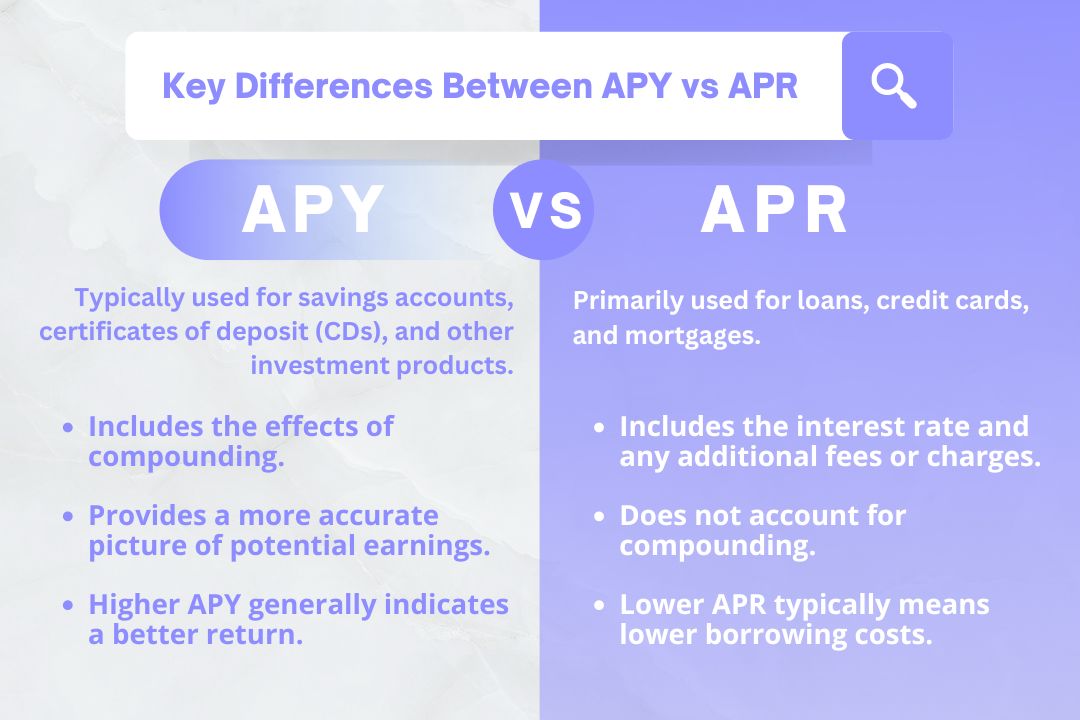

APY vs APR: APY includes compounding and is used for investments, while APR doesn’t and is used for borrowing.

APY (Annual Percentage Yield) and APR (Annual Percentage Rate) are both used to express interest rates, but they calculate and represent these rates in distinct ways that can have a substantial impact on your finances.

Knowing the ins and outs of APY vs APR can help individuals make informed choices about credit cards, loans, and savings accounts. This article aims to break down these concepts, explaining how they differ and why it matters for your financial well-being. We’ll explore how APR affects loans and credit cards, how APY influences savings and investment returns, and provide insights to help you navigate the complex world of interest rates with confidence.

What’s APY (Annual Percentage Yield)?

Annual Percentage Yield (APY) is a key concept in finance that represents the total amount of interest earned on an account over a year, taking into account the effects of compound interest. It’s expressed as a percentage and provides a more accurate picture of the real rate of return on savings accounts, certificates of deposit (CDs), and other deposit accounts.

| Bank Quote (APR) | Annually (APY) | Semi-annually (APY) | Quarterly (APY) | Monthly (APY) |

|---|---|---|---|---|

| 6% | 6% | 6.09% | 6.14% | 6.17% |

| 8% | 8% | 8.16% | 8.24% | 8.30% |

| 12% | 12% | 12.36% | 12.55% | 12.68% |

Unlike simple interest rates, APY factors in the frequency of compounding, which can significantly impact the overall earnings. This makes APY a valuable tool for comparing different financial products, as it standardizes the rate of return and helps in making well-informed decisions about savings and investments.

What’s APR (Annual Percentage Rate)?

Annual Percentage Rate (APR) represents the yearly cost of borrowing money. It includes the interest rate plus any additional fees charged by the lender, such as origination fees and closing costs. APR gives borrowers a more comprehensive view of the total cost of a loan or credit card.

For most loans, the APR is higher than the interest rate because it factors in these extra costs. However, in the case of credit cards, the APR and interest rate are typically the same, as credit card APRs don’t include additional fees like annual fees or balance transfer fees .

Types of APR

There are several types of APRs that borrowers should be aware of:

- Fixed APR: This rate remains constant throughout the loan term, providing predictable monthly payments.

- Variable APR: This rate can fluctuate based on market conditions, often tied to a benchmark like the prime rate.

- Purchase APR: This is the rate applied to regular purchases made with a credit card.

- Cash Advance APR: Usually higher than the purchase APR, this rate applies when borrowing cash from a credit card.

- Balance Transfer APR: This rate is charged when transferring a balance from one credit card to another.

- Introductory or Promotional APR: Often a low or 0% rate offered for a limited time to attract new customers .

Understanding these different types of APRs can help borrowers make informed decisions about their credit options and choose the best fit for their financial needs.

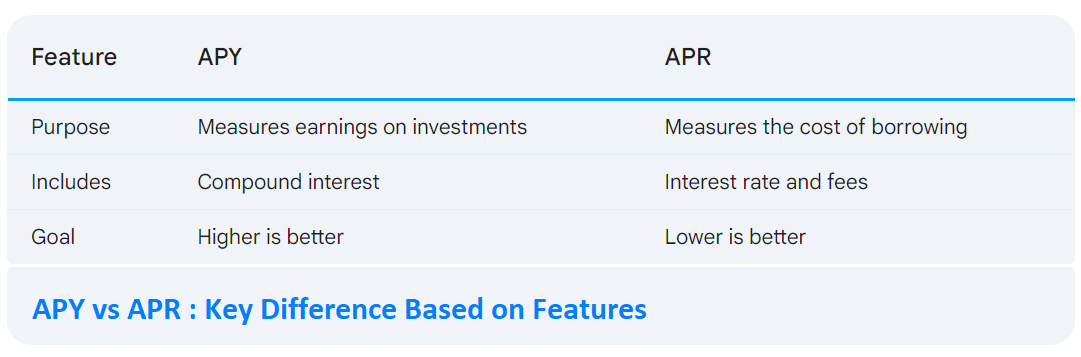

Key Differences Between APR vs APY

The main distinction between APR (Annual Percentage Rate) and APY (Annual Percentage Yield) lies in how they calculate interest and their application in various financial products. Understanding these differences is crucial for making informed decisions about loans, credit cards, and savings accounts.

Interest Calculation Method

APR and APY differ significantly in their approach to interest calculation. APR uses the simple interest method, which multiplies the standard daily interest rate by the number of days in the period. This method does not account for compound interest, making it a straightforward representation of the cost of borrowing .

On the other hand, APY employs the compound interest method. This approach considers not only the initial deposit but also the interest earned in previous periods. As a result, APY provides a more accurate picture of the actual returns on savings or investments over time .

The impact of compound interest becomes more pronounced as the frequency of compounding increases. For instance, daily compounding will result in a higher APY compared to monthly or annual compounding, even if the stated interest rate remains the same .

Application in Financial Products

APR is commonly used in lending products such as loans, mortgages, and credit cards. It represents the total annual cost of borrowing, including interest and additional fees. Lenders are required by the Truth in Lending Act to disclose the APR, making it easier for borrowers to compare different loan options .

For credit cards, the APR and interest rate are often used interchangeably, as credit card APRs typically don’t include additional fees like annual fees or balance transfer fees .

APY, however, is more frequently associated with savings and investment products. Banks and financial institutions use APY to advertise interest-earning accounts such as savings accounts, money market accounts, and certificates of deposit (CDs). The higher the APY, the more interest an account holder can earn over time .

When comparing financial products, it’s essential to consider whether APR or APY is more relevant. For borrowing, a lower APR is generally better as it indicates lower costs. For savings and investments, a higher APY is preferable as it signifies greater returns on your money .

APR vs APY: How Each Affects Your Savings?

When it comes to savings accounts, understanding the difference between APR and APY is crucial. APY, or Annual Percentage Yield, represents the total amount of interest you can earn on your savings over a year, including the effects of compound interest. On the other hand, APR, or Annual Percentage Rate, is typically associated with loans and credit cards, representing the cost of borrowing money.

For savings accounts, APY is the more relevant measure. It takes into account the frequency of compounding, which can significantly impact your earnings. The higher the APY, the more interest you can earn on your savings . For example, if you deposit USD 10000.00 into a savings account with a 4% APY, you could earn more than USD 400.00 after a year .

Compound interest is a key factor in APY calculations. It means you earn interest not only on your initial deposit but also on the interest accumulated over time. This compounding effect can lead to faster growth of your savings, especially over longer periods .

APR vs. What You Actually Get

While APR is primarily used for loans and credit cards, it’s essential to understand its relationship with APY in the context of savings. APR doesn’t account for compound interest, making it a less accurate representation of what you’ll actually earn on your savings .

For instance, a savings account might advertise a 5% APR, but if interest is compounded monthly, the actual APY would be slightly higher at 5.116% . This difference may seem small, but it can add up over time, especially with larger deposits or longer savings periods.

It’s important to note that banks and investment companies generally advertise the APY for savings products, as it provides a more complete picture of potential earnings . When comparing savings accounts, always look at the APY rather than the simple interest rate or APR to get a true understanding of how much your money can grow.

Remember, APY can be variable, meaning it may fluctuate with market conditions or changes in the Federal Reserve’s policies . Therefore, it’s wise to regularly review and compare APYs across different financial institutions to ensure you’re getting the best returns on your savings.

APR vs APY: How Each Affects Your Loans?

When it comes to loans, understanding the difference between APR and APY is crucial for making informed financial decisions. APR, or Annual Percentage Rate, is the standard measure used to represent the cost of borrowing money. It includes the interest rate plus any additional fees charged by the lender, such as origination fees and closing costs .

For most loans, the APR is higher than the interest rate because it factors in these extra costs. This makes APR a more comprehensive representation of the total cost of borrowing. For example, a USD 10000.00 loan with a 10% interest rate, a 1% origination fee, and a 5-year loan term would have an APR of 10.43% .

The Truth in Lending Act requires lenders to disclose the APR when offering credit, making it easier for borrowers to compare different loan options. When shopping for loans, it’s generally advisable to look for lower APRs, as this indicates a lower overall cost of borrowing .

APR vs. What You Actually Pay

While APR provides a standardized way to compare loan costs, it’s important to understand that what you actually pay may differ. This is because APR calculations typically assume that you’ll keep the loan for its entire term and don’t account for the effects of compound interest .

In reality, many borrowers may pay off their loans early or make extra payments, which can affect the total cost of borrowing. Additionally, some loans may have variable APRs that can change over time based on market conditions or other factors .

It’s also worth noting that for credit cards, the APR and interest rate are often the same, as credit card APRs typically don’t include additional fees like annual fees or balance transfer fees . However, credit cards may have multiple APRs for different types of transactions, such as purchases, cash advances, or balance transfers .

When comparing loans, it’s essential to consider not only the APR but also the loan term, repayment schedule, and any potential for rate changes. For long-term loans like mortgages, even small differences in APR can result in significant variations in the total amount paid over the life of the loan 4.

Bottom Line

Understanding the differences between APR and APY has a significant impact on making smart financial choices. APR gives a clear picture of borrowing costs for loans and credit cards, while APY shows the actual returns on savings accounts and investments. This knowledge empowers individuals to compare financial products effectively and make decisions that align with their goals.

To wrap up, being aware of how APR and APY work can lead to better money management. When borrowing, looking for lower APRs can help reduce costs, while seeking higher APYs for savings can boost returns. By keeping these concepts in mind, people can take control of their finances and work towards a more secure financial future.

FAQs

Written by:

Lucy Park is a seasoned writer and editor with a passion for guiding readers towards financial success. Her expertise in investment rates, savings accounts, and saving growth strategies makes her an invaluable asset to our blog.

Reviewed by:

Liam Gray is a dynamic financial analyst and tech enthusiast who brings a fresh perspective to the world of personal finance and investment.